Blogs

What's New Trending

In times of uncertainty, people often look for safe and practical ways to preserve liquidity and park their cash.

There are four common options worth understanding: high-yield savings accounts, certificates of deposit, money market funds, and U.S. Treasuries or Treasury bonds. Each offers a different balance of liquidity, safety, yield, and flexibility.

Understanding how these savings vehicles work can help you make more informed financial decisions and choose the option that best fits your goals.

A high-yield savings account is a savings account that pays a meaningfully higher interest rate than a traditional savings account. These accounts are commonly offered by online banks and digital financial institutions, which often have lower operating costs than traditional branch-based banks. Those lower costs can allow them to offer more attractive yields to customers.

The biggest advantage of a high-yield savings account is liquidity. Your money is not locked up for a fixed term. In most cases, you can deposit funds today and withdraw them whenever you need them, making this a practical option for emergency funds, short-term savings, or cash you may need to access quickly.

However, one important point to remember is that the interest rate on a high-yield savings account is usually variable. The rate can change based on market conditions and the bank’s own decisions. That means if you move a large amount of cash into a high-yield savings account because it is paying 5%, you should not assume that rate will stay there. It could go down in the next few days or weeks. It could also go up, but the key point is that the rate is not guaranteed.

There are two important things to watch carefully with high-yield savings accounts.

First, make sure the bank is FDIC-insured. FDIC insurance protects eligible bank deposits up to $250,000 per depositor, per insured bank, per ownership category, which is why it is important to confirm that the institution holding your money is actually covered.

Second, be careful with advertised rates that look unusually high. Sometimes you may see a savings account advertised at a rate that is significantly higher than the market rate. For example, if most high-yield savings accounts are paying around 4%, you may see an ad promoting 6%. There is often a catch. The higher rate may apply only for the first month, only up to a certain balance, or only if you meet specific conditions.

As a general rule, if a rate looks much higher than what the rest of the market is offering, pause before moving your money. Banks cannot usually pay significantly above-market rates without some limitation, condition, or promotional structure attached. A high-yield savings account can be an excellent place to park cash, but only when you understand the actual rate, the conditions attached to it, the safety of the institution, and the fact that the rate can change over time.

A certificate of deposit, commonly called a CD, is another cash parking option offered by many banks and credit unions. The main differences between a CD and a high-yield savings account are liquidity and rate certainty. With a high-yield savings account, you can generally access your money whenever you need it, but the interest rate is usually variable and can change based on market conditions. With a CD, you agree to keep your money deposited for a specific period of time, such as three months, six months, one year, or longer. In return, the bank typically offers a fixed interest rate for that term, which can be useful if you want more predictability or if you believe interest rates may decline in the near future.

Technically, you can often withdraw your money before the CD matures, but doing so usually comes with an early withdrawal penalty. The exact penalty depends on the bank and the specific CD terms. Federal rules set a minimum penalty for certain early withdrawals, but there is no maximum penalty, so the account agreement matters.

In practical terms, this means you may not receive the full advertised return if you break the CD early. In some cases, the penalty can reduce or even eliminate the interest benefit you expected from the CD. That is why CDs are generally better suited for money you are reasonably confident you will not need during the term.

As mentioned earlier, FDIC insurance is still important, especially when parking larger amounts of cash. But the bigger practical question with CDs is simple: Can you afford to leave this money untouched until the CD matures? If the answer is yes, a CD may offer a predictable return. If the answer is no, a high-yield savings account may be a better fit.

A money market fund is a type of mutual fund designed to invest in short-term, relatively low-risk securities. These investments may include Treasury bills, government securities, municipal debt, high-quality corporate debt, and other short-term instruments. The goal is usually to provide liquidity, preserve capital, and generate a modest return. The SEC’s investor education site describes money market funds as mutual funds that invest in liquid, short-term debt securities, cash, and cash equivalents.

This is slightly different from a bank account. A high-yield savings account or CD is usually offered by a bank or credit union. A money market fund is usually offered through a brokerage firm or mutual fund company, such as Fidelity, Vanguard, or Schwab. In many brokerage accounts, uninvested cash may automatically sit in a “core” or settlement position, which may be a money market fund or another cash sweep vehicle. Fidelity, for example, explains that opening an account automatically establishes a core position used for cash transactions and holding uninvested cash.

The main advantage of a money market fund is flexibility. Your money is generally not locked up for a fixed term. You can typically withdraw money, move it, or use it to buy investments in your brokerage account. In that sense, money market funds behave more like high-yield savings accounts than CDs.

However, money market funds are still investments, not bank deposits. They are generally considered very low risk compared with most mutual funds, but they are not FDIC-insured. The FDIC specifically notes that mutual funds are not insured by the FDIC, even if purchased through an FDIC-insured bank.

If a money market fund is held in a brokerage account, it may receive SIPC protection. But SIPC protection is not the same as FDIC insurance. SIPC generally protects customers if a brokerage firm fails and customer securities are missing; it does not protect you from investment losses or guarantee the fund’s yield. FINRA explains that SIPC protection covers missing securities and cash in eligible brokerage accounts, but it is not protection against market loss.

Treasury securities are issued by the U.S. government. In simple terms, when you buy a Treasury bill, note, bond, or Series I Savings Bond, you are lending money to the federal government and receiving interest in return.

The main advantage is tax treatment. Treasury interest is generally subject to federal income tax, but it is exempt from state and local income taxes. This can be especially useful for investors in high-tax states such as California.

For short-term cash parking, many people look at Treasury bills, which are issued for terms ranging from 4 weeks to 52 weeks. They are usually sold at a discount, and when they mature, you receive the full face value. You can buy Treasury bills, notes, bonds, TIPS, and other Treasury securities directly at TreasuryDirect.gov. Many brokerage firms, including Fidelity and Vanguard, also allow investors to buy Treasury securities through brokerage accounts.

Liquidity depends on what you buy. Treasury bills, notes, and bonds are marketable, which means they can generally be sold before maturity. However, if you sell before maturity, the price may be higher or lower than what you paid depending on interest rates at that time. If you want simplicity, many investors buy shorter-term Treasury bills and hold them until maturity.

Series I Savings Bonds, commonly called I Bonds, are a little different. They are designed to protect against inflation. Their rate has two parts: a fixed rate that stays with the bond, and an inflation-based rate that changes every six months. So the yield is variable, not fixed.

I Bonds also have stricter liquidity rules. You cannot cash them in during the first 12 months. If you cash them in before five years, you lose the last three months of interest. After five years, there is no early redemption penalty. Like other Treasury securities, I Bond interest is generally exempt from state and local taxes, and federal tax can usually be deferred until you redeem the bond.

Treasury securities can be useful for cash parking because they are backed by the U.S. government and offer state and local tax advantages. But the right choice depends on your time frame. Treasury bills may work well for shorter-term cash parking, while I Bonds can be useful for inflation protection if you are comfortable with the 12-month lockup.

These are some of the most commonly used ways to park cash during uncertain times. Each option works differently, and each comes with its own trade-offs around liquidity, rate certainty, safety, taxes, and access.

The goal is not to declare one option as the best. The goal is to understand how these cash parking vehicles compare, so you can evaluate which one fits your specific situation.

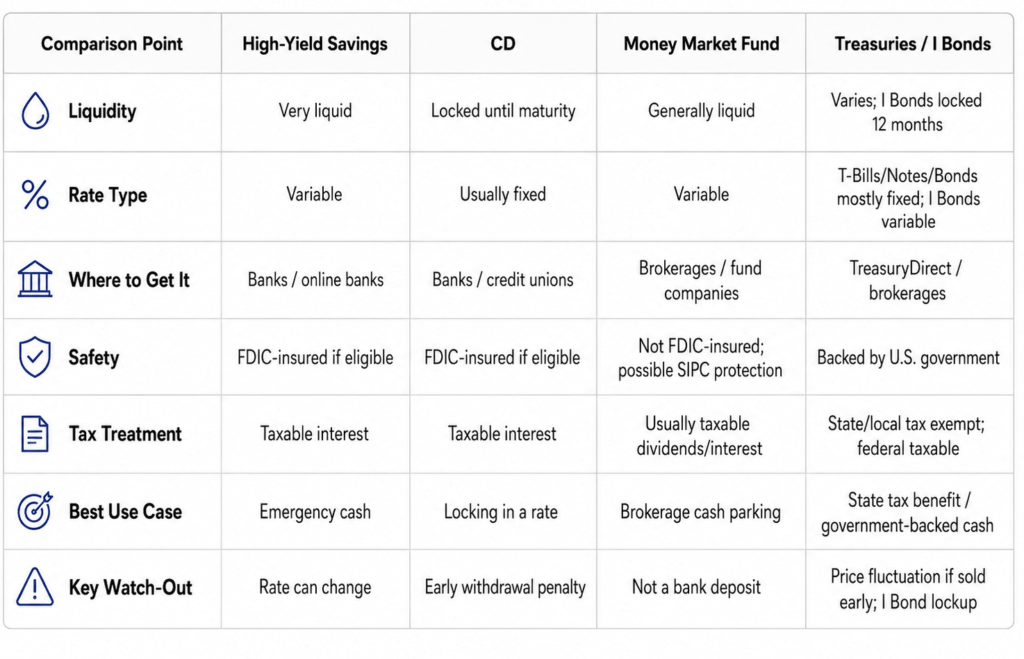

The table below summarizes the key differences.

Leave a Reply